Is it really worth getting pet insurance for older pets? I’ve seen a lot of people saying it’s not worth it and that you’re better off putting the money into savings. Just curious about everyone’s thoughts, especially since here are the lifetime costs I’ve spent on my dachshund.

7 Likes

Honestly, no matter what people say, having pet insurance gives you peace of mind. Even though you hope you never need it, it’s good to have. I’ve got insurance for my Frenchie ![]() .

.

7 Likes

The problem comes with the way they hike up prices. Pet insurance is great when your dog’s young, but they start raising the prices so high as your dog gets older. Like, if your dog lives till 15 or more, you could be paying $500-600 a month. The longer they live, the more expensive it gets, and eventually, it just becomes unaffordable.

6 Likes

That’s true for some, but it really depends on the company and your plan. My Yorkie lived until she was 16, and we were paying around $250 a month with Embrace. I’m in California, which isn’t exactly cheap either.

That’s true for some, but it really depends on the company and your plan. My Yorkie lived until she was 16, and we were paying around $250 a month with Embrace. I’m in California, which isn’t exactly cheap either.

What worked for us was starting a policy when the dog was young, getting the best coverage possible with a low deductible and high reimbursement rate. As she aged, we put money into savings and adjusted the policy by increasing the deductible and lowering the reimbursement to keep premiums down. That way, we used the savings to cover the higher deductible and still kept the coverage.

I get that insurance costs more as pets age, but it’s better than being wiped out financially if something happens. You could reach a point where it’s no longer worth it, but every situation’s different. For my senior Yorkie, $3k a year was manageable, especially considering her expensive meds and specialist care. It was totally worth it for us ![]() .

.

4 Likes

My dog’s only 10, and I’m already paying $200 a month. It’s been going up about $50 every year for the past few years. If it keeps climbing at this rate, I’ll be paying $500 or more by the time he’s 15. That’s $6k a year, which is just crazy.

3 Likes

Does that $46k total include the annual deductibles and the 10-30% copays? Were there any claims denied? Also, what about the costs for routine care that insurance doesn’t cover?

I just did a forecast for my two kittens’ healthcare costs for the next 15 years. I figured it’d be about $30k total, assuming I go with a good carrier that doesn’t drop coverage after they turn 12. I also looked at putting money into savings, $10k saved now could grow into $40k after 15 years, as long as I don’t have to dip into it.

I’m thinking about doing both high-deductible insurance and self-insuring. That way, if they stay healthy, I’ll have money left over. And if they get sick or insurance falls short, I’ll have extra money to cover things like dental cleanings or the parts insurance doesn’t touch ![]() .

.

3 Likes

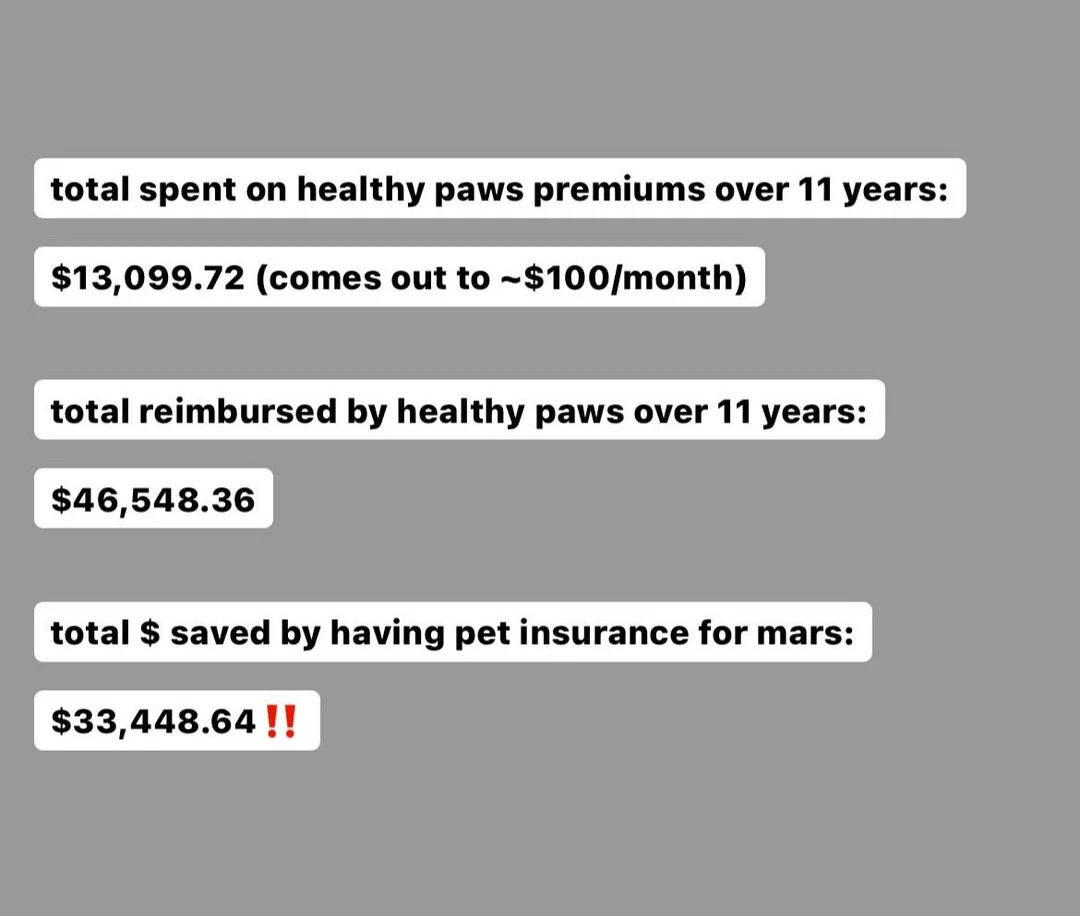

No denied claims. I got the insurance when my dog was a puppy, so there weren’t any pre-existing conditions. We started paying $34.50 a month in 2013, and by the time he passed this year in 2024, it was up to $238.16 a month.

That $46k is what they reimbursed 90% of the costs for 195 claims over 11 years. We still paid around $4,600 out of pocket, plus exam fees, which weren’t covered.

Routine stuff not covered included things like Bravecto ($75 every three months) and prescription food ($50 a month). Dental cleanings weren’t covered either, so we paid a couple of thousand dollars for those.

We also used Healthy Paws for a kitten who sadly got cancer at six months old. He lived for 18 months, and they reimbursed almost $50k for all his treatments, even though his premium was only around $19 a month. So, for those worried about premiums going up due to claims, that wasn’t our experience. They raised it annually across the board but not because of our claims.

3 Likes

But your dog passed at 11, so you didn’t deal with the crazy pricing. Insurance is amazing if your pet passes young, but if they live into their teens, the premiums get too high. It’s better to put the money into savings once your pet is older because, by the time they hit 15-18, you’ll be paying $6-10k a year.

So yeah, insurance is great for younger pets or breeds with shorter lifespans. But if you have a smaller breed, once the premium reaches $3-4k a year, you might as well save that money instead.

3 Likes

I’m doing something similar. I’ve been putting money into a high-yield savings account because I’m not too familiar with Trupanion’s lifetime deductible structure. If things get too expensive, I’ll probably raise the deductible to keep premiums down and use savings for the rest, like dental care and wellness.

I’ve got insurance because I know I’ll need it eventually, given my breed’s health concerns. But building up savings and having insurance seems like the best strategy these days ![]() .

.

2 Likes

You’re going to spend money on copays and deductibles with or without insurance, so leaving that out makes sense.

1 Like

And what about denied claims?

1 Like

Denied claims don’t change the fact that premiums vs. payouts are what really matter. Even if there were $100k in denied claims, the savings from the insurance would still be the same. Denied claims are more relevant when comparing insurance plans, not whether to get insurance in the first place.